What is Sharpe Ratio?

The Sharpe ratio is a way to measure investment and portfolio performance. It compares the performance of a portfolio to a risk-free asset, and adjusts for the amount of risk inherent in the investment. A high-quality portfolio will have a sharpe ratio greater than 0.8, and a low-quality one will be below 1.0. This is a good indicator for investors who want to maximize their returns.

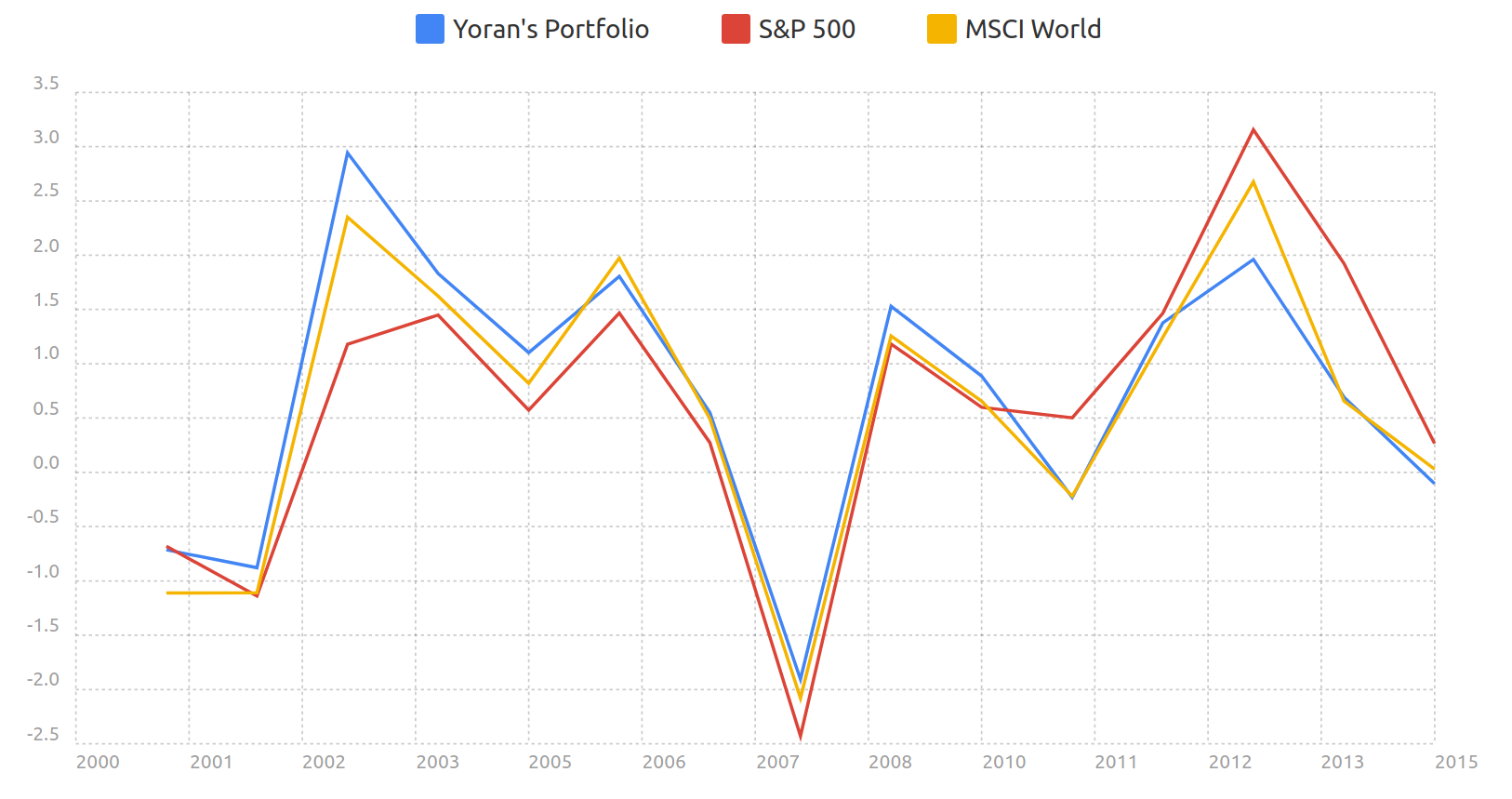

Sharpe Ratio:

The Sharpe ratio is often used by individuals who add new financial instruments to their portfolio, but want to know if the new investments will increase their risk-reward profile. The standard deviation of daily returns is higher than for weekly and monthly returns, and the calculation is based on the assumption that all price movements are equal. The annualized standard deviation of weekly and monthly returns is higher, because the volatility of daily returns is larger than for monthly or yearly returns.

The Sharpe ratio is most useful when comparing portfolios with similar risk-return characteristics. For example, if two portfolios have the same average monthly return, but one has more volatile returns, the Sharpe ratio of Strategy B would be higher. While the Sharpe Ratio can be useful for determining which is a better investment, it may not be appropriate for every type of portfolio. The following examples are based on the most commonly used portfolios with low risks and high return profiles.

The Sharpe ratio is a metric for measuring risk-return relationships. It measures whether an investment’s returns are the result of savvy investment selection or over-risk. Increasing the Sharpe ratio will improve the likelihood that a fund will achieve its objectives. For instance, modern portfolio theory suggests adding more low-risk assets to a diversified portfolio to reduce its volatility and increase the Sharpe ratio. The assumption is that volatility is equal across different asset classes, so a high-risk investment will generate a higher Sharpe ratio than a low-risk one.

When analyzing risk-return characteristics of two investments, Sharpe Ratio can be an effective tool for comparing the risks of different types of assets. For example, if a security has a risk-free rate of 5%, the Sharpe ratio for the same investment will be 0.2, and vice versa. If you want to maximize your returns, the Sharpe-ratio is an essential metric in evaluating the risks and rewards of new investments.

Sharpe Ratio useful tool:

The Sharpe ratio is a useful tool for evaluating investment risk and return. To calculate the Sharpe ratio, divide the total rate of return of your portfolio by the risk-free rate. This value is known as the risk-free rate. This value is the excess return of an investment over a long period of time. The risk-free rate is the return over the same level of U.S. Treasury bonds. In addition, the ratio will help you determine the risk-free investment for your individual needs.

The Sharpe Ratio is a common tool for investors, which is calculated by taking the risk-free rate of an investment and dividing that by the standard deviation of its portfolio’s returns. By looking at the Sharpe ratio, you can determine the overall risk-free rate of an investment. A high Sharpe ratio means that the investment is risk-free. However, this is not intuitive, but it can help you understand the risk-free rate of an investment.

The Sharpe ratio can be useful for determining whether an investment is a good choice. The standard deviation is the difference between the risk-free rate and the return. This means that the higher the standard deviation, the better the investment. A lower Sharpe ratio means that you should be careful when investing. If you want to maximize your profits, you need to understand the risks and the returns of an investment. Fortunately, there are many factors that will affect the Sharpe factor.

The Sharpe ratio is calculated by subtracting the risk-free rate from the expected return of an investment and dividing it by the portfolio’s standard deviation. For example, an investment that yields a 6% return would have a Sharpe ratio of 1.0. Its risk-free rate would be 1.0%, and its standard deviation would be 5%. This is a pretty good indicator of how well an investment is doing, as it will likely be more profitable if it has a lower standard deviation.